Allocation Round 6 (AR6) has awarded 5.4 GW of offshore energy contracts, across fixed and floating offshore wind and tidal stream. Here, Grace Millman digs into the winners of today's auction to explore what it means for the offshore sector.

Allocation Round 6 (AR6) has awarded 5.4 GW of offshore energy contracts, across fixed and floating offshore wind and tidal stream. Here, Grace Millman digs into the winners of today's auction to explore what it means for the offshore sector.

After last year’s disappointment with AR5, which failed to secure any bids from offshore wind developers, today’s news of a successful AR6 auction will be welcomed by the industry as a big step forward in delivering clean, renewable energy. You can check out our interactive map of the winners across all technologies here.

This year’s Contracts for Difference (CfD) auction has secured 4.9 GW of fixed offshore wind, 400 MW of floating offshore wind and 28 MW of tidal stream energy through 16 projects across England, Scotland and Wales. Among the winners were Hornsea Four, 2.4 GW of fixed offshore wind off the Yorkshire coast, Green Volt (400 MW), the first floating project to come through Scotland’s Innovation and Targeted INTOG round, and a further 9 MW of tidal stream at MeyGen in Scotland. Notably, AR6 included 1.6 GW of fixed offshore wind via ‘permitted reductions’ – a scheme that allowed projects previously awarded a CfD contract to withdraw up to 25% of their original capacity and apply to a future CfD round.

It will have been high on Labour’s list to deliver a successful CfD round in its first 100 days in power. The previous government increased the Administrative Strike Prices (ASPs) for this round, reflecting the rise in supply chain and construction costs over the last 24 months, and Labour increased the overall budget from £1.1bn to £1.5bn. It was expected that the increased budget could secure between 5-6 GW of new fixed offshore wind projects. In the end, the auction delivered 4.9 GW of offshore wind capacity, although just over 1.5 GW was via the ‘permitted reduction’ route, leaving 3.3 GW for two new projects.

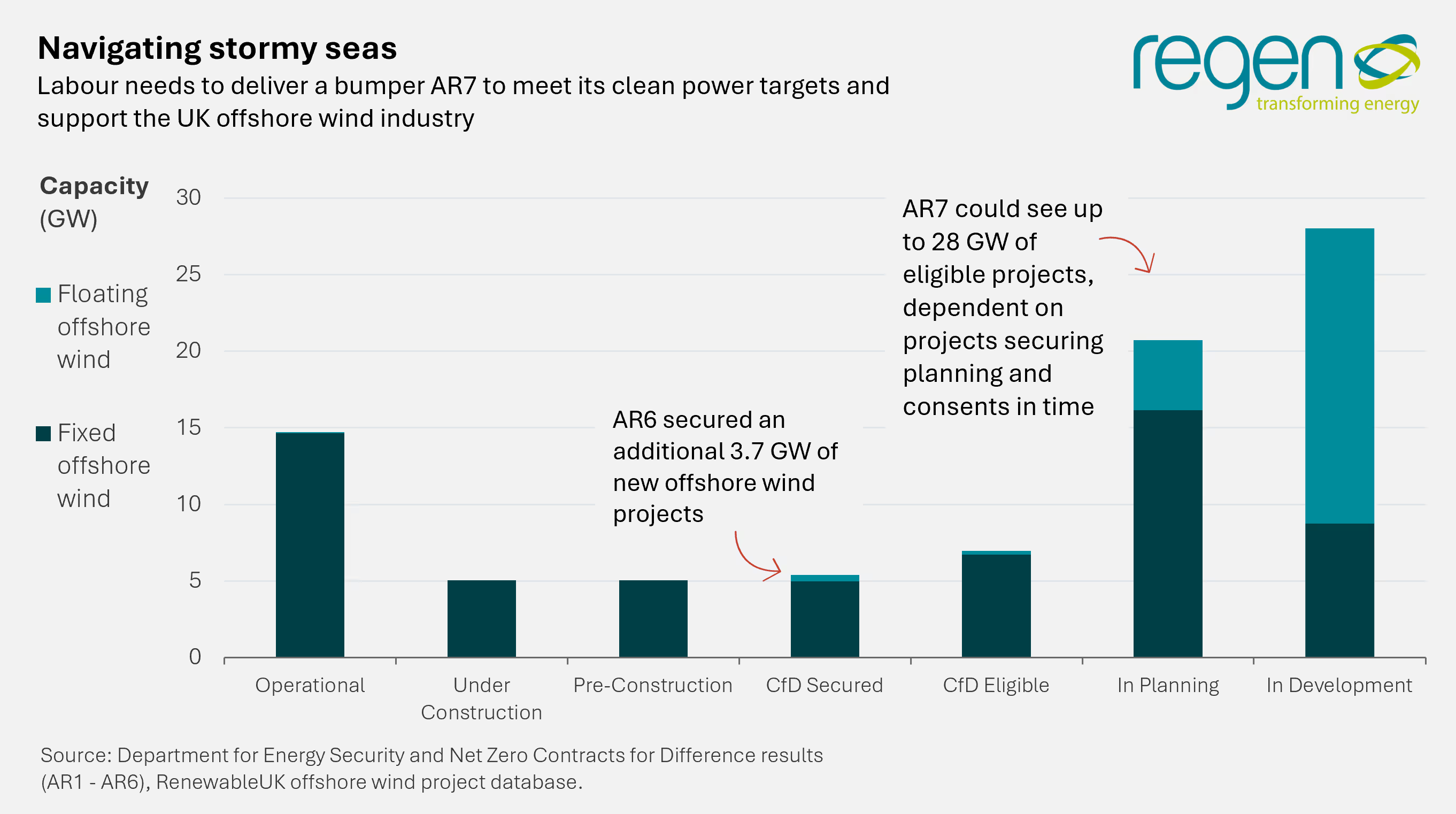

This means that a number of eligible offshore wind projects missed out. We don’t know which projects submitted a bid, but there were estimated to be c. 8 – 12 GW of CfD-ready projects in the fixed offshore wind pipeline. So we can surmise that AR6 was a very competitive auction round – hence the low auction strike price well below the government’s maximum administrative strike price of £73 per MWh. This also means that there will be capacity available to bid into AR7, which is increasingly looking like the ‘big one’ to meet the government’s clean power target.

Of the five fixed offshore wind projects that were awarded CfDs during AR4, four of these took advantage of the CfD ‘permitted reduction’ mechanism, which allowed them to withdraw up to 25% of their original capacity and bid again into AR6, securing a £16.88/MWh uplift for this capacity. The only project that didn’t re-bid was Norfolk Boreas, which paused development last year due to soaring costs. As so many projects bid under this category, totalling 1.6 GW, the scope for new fixed offshore wind projects was significantly reduced, with only two new projects securing CfDs. These were Hornsea Four (2.4 GW) and East Anglia Two (963 MW). We believe that there was between 5 GW and 9 GW of eligible fixed offshore wind projects which might have bid and not secured contracts today.

This round was also an opportunity for developers to make competitive bids, giving an indication of what is a realistic development price within the current market. The auction landed on strike prices of £58.87/MWh for fixed offshore wind (quoted in 2012 prices), well below the ASP of £73/MWh. This is a very positive outcome and credit should go to government officials and industry who have worked together to find a price that delivers value for money to the consumer as well as a fair return on investment for developers. The government should use this experience to understand that a ‘race to the bottom’ is not the way to create a sustainable industry.

The floating offshore wind industry welcomed the increase in ASPs to £176/MWh; however, noted that the budget of £270m for Pot 2, shared across a number of emerging technologies, would not be enough to support more than one or two projects. It has been confirmed today that AR6 has supported only one floating offshore wind project: GreenVolt, which is part of the Scottish INTOG leasing round. With only one floating offshore wind project previously successful through the CfD, seeing 400 MW secure a contract is a positive step forward for the sector.

It is understood that there were four eligible projects for this round, including key Test & Demonstration (T&D) projects like Erebus in the Celtic Sea. It was expected that these floating offshore wind projects would bid close to the ASP; however, GreenVolt secured a contract at £139.93/MWh (quoted in 2012 prices). As part of INTOG, GreenVolt’s business model includes delivering renewable electricity to oil and gas platforms off the Peterhead coast, while also delivering renewable electricity to the UK grid. GreenVolt’s larger size and ability to access different revenue streams may have allowed it to achieve a lower strike price than the other eligible floating offshore wind projects.

Floating offshore wind is now recognised as a significant part of the UK’s future energy mix; however, only 236 MW is currently installed worldwide. T&D projects provide crucial stepping stones for the industry to de-risk technology, provide confidence to the supply chain and enable cost certainties in competitive auction rounds. Before the leap is made to GW-scale projects in the Celtic Sea and through ScotWind, we need to give the supply chain and the industry a chance to expand into this new sector, as well as having sufficient lead times to allow the industry to respond to the learnings from the T&D sites. Therefore, it is important that we get as many of these projects out to sea as rapidly as possible.

Competition is the name of the game when it comes to CfDs. However, due to its early-stage development, many question whether this is appropriate to stimulate strategic investment in floating offshore wind. The focus on cost competitiveness means that these smaller T&D projects are likely to lose out to larger eligible projects, as evident in today’s results. Previous floating offshore wind T&D sites (namely Kincardine and Hywind Tampen) have been supported by Renewable Obligation Certifications (ROCs), the government’s previous revenue support mechanism. A specific ‘hurdle’ CfD strike price for T&D sites, allowing projects to access a CfD outside the main auction, would recognise the importance of these projects as a catalyst for future development, ensuring that the CfD can act strategically to procure capacity where it delivers the most impact.

The tidal stream industry has steadily developed in recent years and today’s announcement demonstrates the ongoing appetite to invest.

The increase in budget for Pot 2, with a £15m ringfence for tidal stream, has supported more tidal projects. After the successes of AR4 and AR5, which resulted in over 90 MW of tidal stream capacity, expectations for AR6 were high. For the third consecutive allocation round, tidal stream secured capacity across multiple projects, including Oceanstar, SEASTAR, Hydrowing, Magallanes and MeyGen, totalling 28 MW across Scotland and Wales. This represents another major step forward for this sector.

As the focus turns to deploying the successful projects from AR4 and scaling up the supply chain to meet demand, the government must continue to nurture tidal stream development and allow the pipeline to develop. Ensuring the success of near-commercial projects is vital for industry confidence and momentum, but less-established players shouldn’t be forced to cut costs at the expense of development. Squeezing the industry in future allocation rounds will stifle the pipeline of projects, which is vital for progressing towards lower energy costs, especially for developers who have just won CfD support.

Labour has course-corrected through AR6, supporting a number of new projects and topping up previous AR4 projects to reflect increasing supply chain costs. However, to meet its own 2030 clean power target, the government needs to continue to rapidly progress the GWs of eligible offshore wind projects. For AR7, the government has greater scope to deliver a bumper round, with more control over the auction parameters. Regen recommends that the government focuses on the following priority areas:

Sign up to receive our monthly newsletter containing industry insights, our latest research and upcoming events.