In our response to the second Review of Electricity Market Arrangements consultation, we welcome the decision to drop nodal Locational Marginal Pricing and a Split Market and recommend now dropping zonal pricing.

In our response to the second Review of Electricity Market Arrangements consultation, we welcome the decision to drop nodal Locational Marginal Pricing and a Split Market and recommend now dropping zonal pricing.

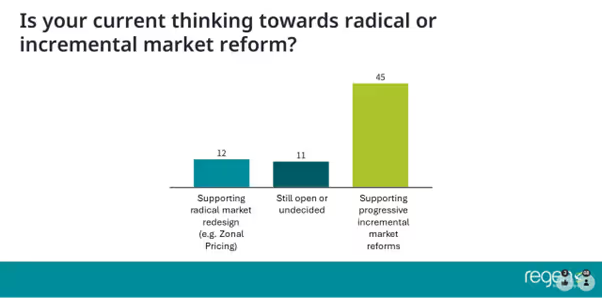

Along with many organisations, Regen has submitted its response to the Review of Energy Market Arrangements (REMA) second consultation.

Our response welcomes the publication of the second REMA consultation as an important milestone towards the development of an efficient GB electricity market and expresses Regen's appreciation of the work done by the REMA team and the progress that has been made.

The response is in two sections:

In most key areas of the Regen response, we are supportive of the overall REMA direction of travel and the options that have been proposed, including the decision to drop nodal Locational Marginal Pricing and a Split Market option.

The main difference of view, which is shared by the majority of companies and organisations working in the energy sector, is a firm recommendation that DESNZ should drop the zonal pricing option to reduce investor uncertainty and enable resources to focus on other more workable solutions.

The rationale to drop zonal pricing, after two years of REMA development, is that:

If DESNZ decides to keep zonal pricing as an option, then a lot more work is needed before any design decision can be made. This additional work includes:

Regen's view is that the benefits of an efficient energy market, and REMA's four challenge objectives, can be better and more quickly achieved through a programme of Progressive Market Reform, based on the foundation of the current national trading market arrangements.

We have set out some of the key pillars of a progressive market reform agenda in our consultation response and will shortly publish a position paper on this subject. Key areas for reform include:

Regen will continue to work with the REMA team and our industry colleagues over the coming months and we welcome any feedback on our consultation response.

The Electricity Storage Network has also submitted a response and Regen has co-authored a response on behalf of 52 local authorities that are participating in the Innovate UK Net Zero Living Thriving Places project.

Sign up to receive our monthly newsletter containing industry insights, our latest research and upcoming events.